Bitcoin, Ethereum, and everything else

Bitcoin, Ethereum, and everything else

Issue #11

Blockchain is really confusing. That's why I write this newsletter.

You hear so many things. Sometimes people say ‘blockchain technology’, other times it's a blockchain or the blockchain.

‘Blockchain technology’ is like saying ‘computer technology’. It describes the general tech, but not a particular example.

Just like Macbook and Thinkpad are examples of computers, Bitcoin and Ethereum are examples of blockchains.

So when people say 'put it on the blockchain' 'The' in this context is referring to a specific blockchain.

The problem is there are 1000's of blockchains. How can one tell which ones are good?

One great metric is transaction fees. These are fees users pay to make a transaction, like sending money from A to B.

If people are paying fees to use the system, it indicates the service is providing them real value.

More importantly, unlike other metrics, transaction fees can’t easily be faked. This is because transaction fees go to people updating the blockchain, an open group outside of the fee payer’s control.

Transaction fees also help you value crypto networks as they are a type of cash flow. If blockchains were a company, transactions would be the product.

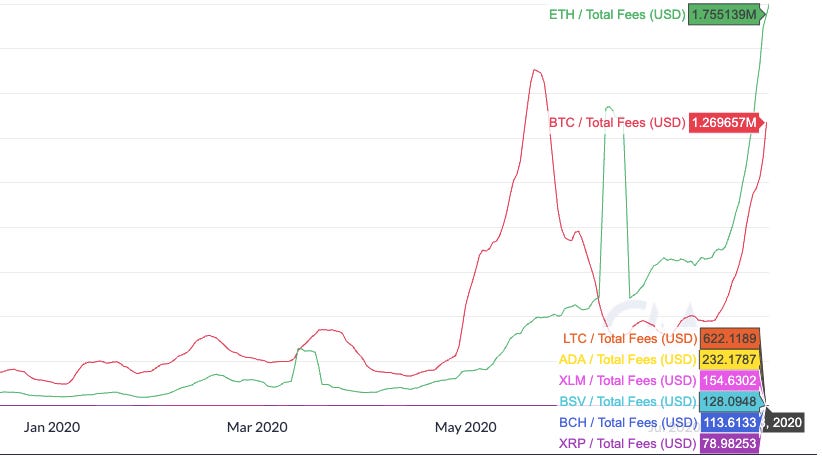

Here are the 7-day moving averages of transaction fees paid across the major blockchains:

Ethereum's currently collecting $1.75m/day in fees, compared to Bitcoin's $1.26m/day.

The rest of the top 10 collect a little more than $1k/day combined.

Bitcoin and Ethereum collect nearly 10,000x more in fees than their closest competitors.

Uniswap, a single app built on Ethereum, recently earned a whopping $443k/day in fees just by itself!

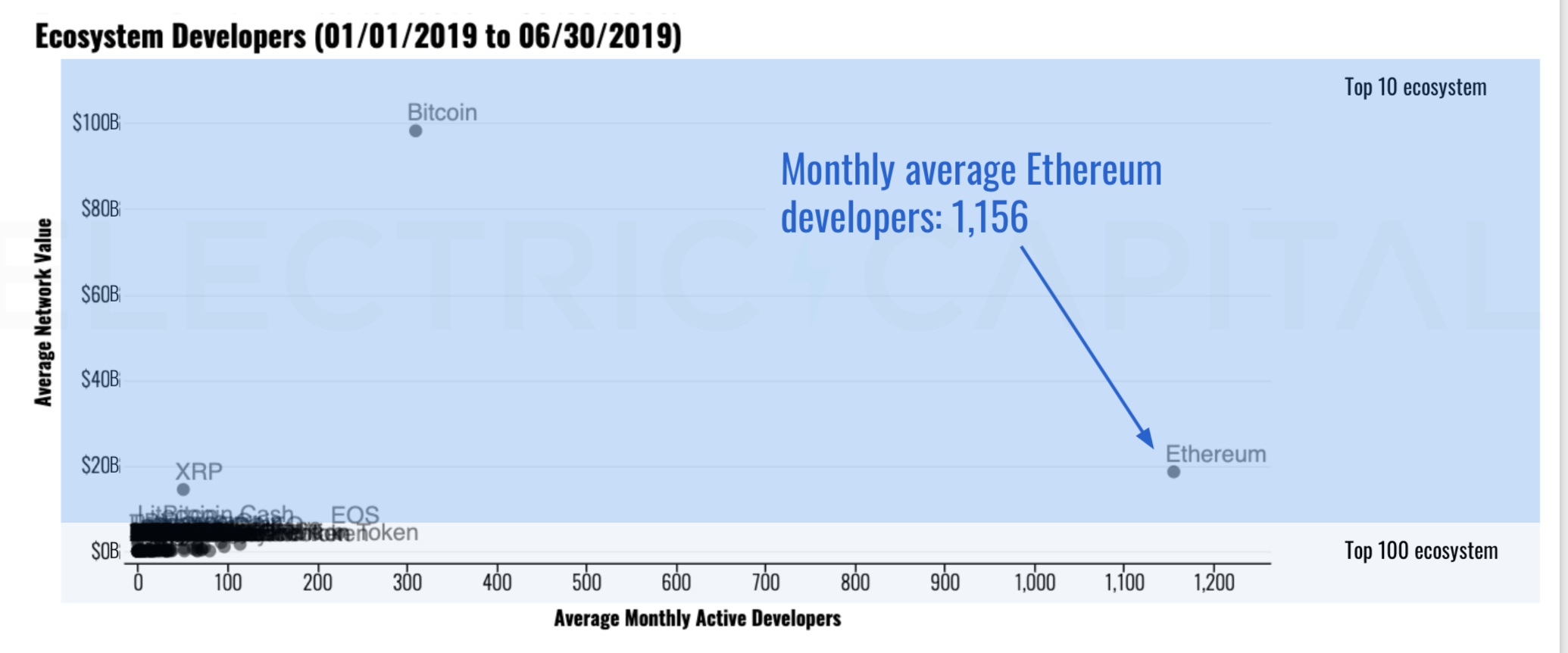

Not only that, but there are far more developers working on apps on Bitcoin and Ethereum than any other blockchain.

This is why when you hear people talk about the blockchain they're usually talking about Ethereum.